Comparing Stock to Real Estate, Apples to Apples

Andrew Campbell

May 10, 2019

Today we continue our series focused on identifying and understanding investment opportunities, as well as the underlying decisions that go into making these investments. Our last article focused on defining what a good return is and discussed comparing various risk profiles of seemingly similar opportunities and how that can impact our understanding of different potential returns.

In today’s article, we’re focusing on how we think about investment opportunities compared across different asset classes–namely real estate vs. the stock market. This article’s comes from our Junior Partner Jeff, and is based on several of his past discussions.

—

As I’ve grown my real estate portfolio and established experience across the industry I’ve had a ton of interest from friends and family following my journey. This interest inevitably leads to conversations about why I’ve taken such a shine to real estate as an asset class, and often friendly debates about real estate’s track record vs other asset classes. One recent conversation with a friend went deep into the pros and cons of real estate vs the stock market, and left us both reaching deep to support our thesis for our preferred investment vehicle–but one of the biggest pain points was truly being able to compare our investments and returns in a true apples to apples way.

Also in case it’s not clear I deeply respect my friend. This guy is one of the smartest and most successful individuals I know and has created disproportionate returns for himself across a variety of investments. He hasn’t had personal experience investing in syndicated multi-family deals however and living in the heart of Manhattan doesn’t have visibility to the types of assets we choose to invest in out here in Texas. I explained how we operate at Wildhorn Capital and how a big focus of our thesis is around quarterly distributions that create passive income for my family. He began to press me on this passive income piece, it’s something he’s focused on also. He asked, “What makes an investment in real estate stronger than an investment in a dividend stock like AT&T, can’t you can expect to receive similar returns?” Good question. As the debate continued, there was only one point I was willing to acquiesce on–stock market investing has more inherent liquidity than real estate as you can pull your money out of the market anytime. There were three main points we focused on, and without the data at our fingertips, walked away with vastly differing opinions on. I wanted to detail those points below with a little more research. These criteria are critical to take a data driven approach to compare, I hope this is a useful tool in analyzing investment opportunities no matter the asset class:

Point #1: What Asset Drives Stronger Quarterly Returns

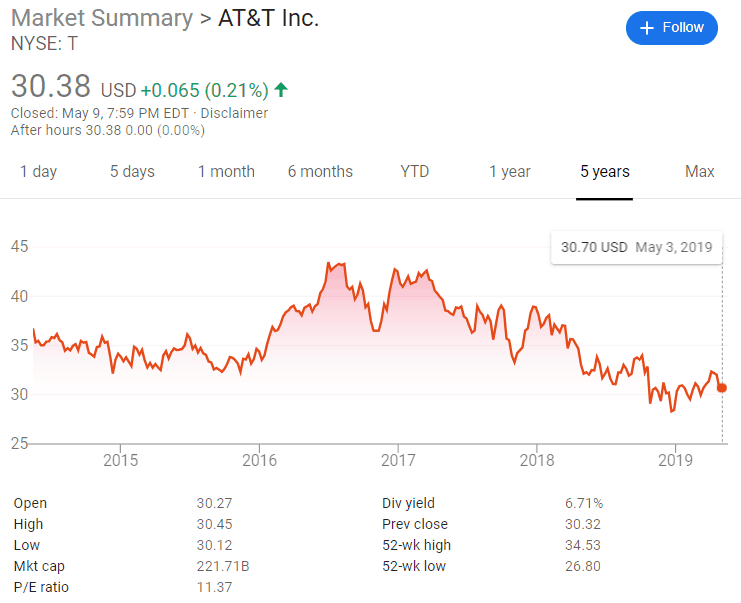

The first thing my friend mentioned was that he could get some of the strongest returns he’s seen in the market by investing in a stock that has an expressed focus of paying dividends to its investors. The stock he had invested in was AT&T. He couldn’t remember the specific dividend yield he received last quarter, so I looked it up. It was 6.34%. Now that’s a strong return in my book, but looking back a bit further the average has actually hovered just over 5%, going as low as 4.35% in recent memory (last 5 years).I compared this to some of the returns I’ve seen on recent syndicated real estate investments, where the average cash on cash returns are 5% to 10%+. In our deals at Wildhorn, we utilize a Preferred Return structure that nets me (as an LP investor) 6%+ returns from our asset’s operating cash flow–and most times those distributions start immediately. A 6% “dividend” from the real estate asset, you have a starting return (on the low end) that performs better than the highest expected return of a dividend stock asset. I view that as having more cashflow upside in real estate. An additional comfort I have, is the structure of the real estate deals we invest in–our management team underwrites deals conservatively, and they don’t get paid until after the preferred return is satisfied. In all of our investments, we’ve seen those low end projections met and/or exceeded. I can’t find a stock investment structure that allows for a similar structure. In fact how often do you see a Fortune 500 CEO getting paid huge amounts of money from some “Golden Parachute” clause despite being fired for driving negative returns for their investors, essentially failing at their job. The answer is way too much.

Point #2: Can you Expect Appreciation

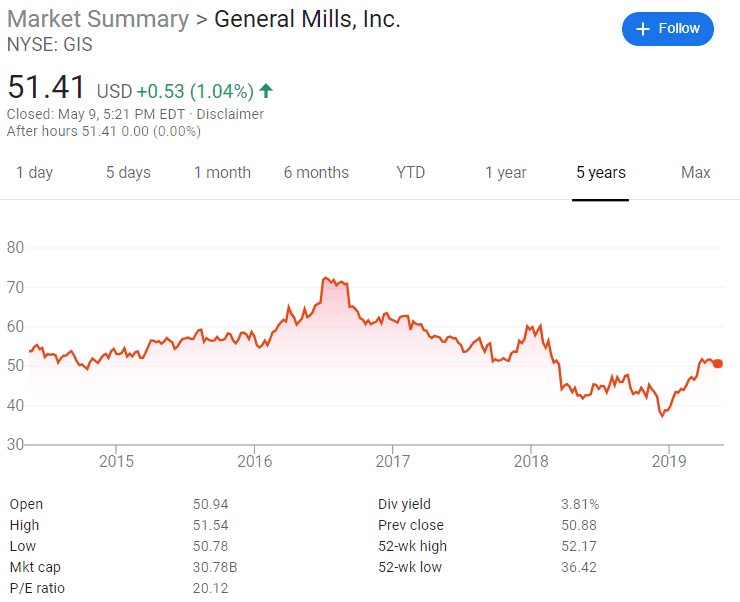

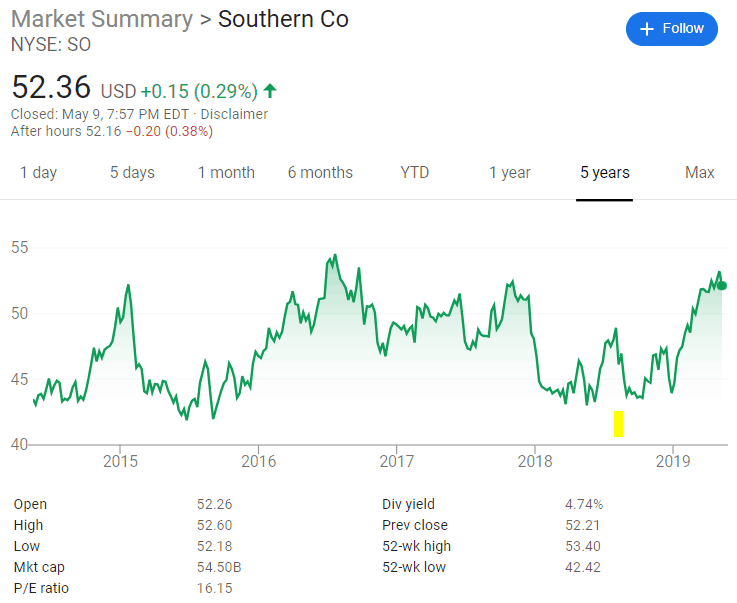

There is a popular real estate quote attributed to Mark Twain that says “Buy Land. They aren’t making any more of it.” That’s the basic idea of appreciation and why real estate is such a simple and attractive asset to many people. Historically, land value goes up in value over time. You can find real estate investments that produce the dividend/cash flow described above, AND see appreciation all along the way. Looking at the AT&T graph above it’s easy to see that over that 5 year period, investors who were holding their breath for much appreciation would pass out and die. From my research this seems like a pretty standard expectation for dividend stocks, trade tomorrow’s growth from appreciation for payouts to investors today. Take a look at a few other examples (CPG, Oil & Gas, Utilities)…

By and large these profitable, established corporations have seen little to no appreciation and instead prioritize paying out returns to their investors.Again, compare this with multifamily value add real estate where the business plan often includes ways to drive appreciation as we investment back into the property. Not only do we expect natural appreciation to occur, but we go into an asset with a plan to force appreciation as we grow the NOI of the property. According to our business plan, the same five year time horizon would have a different trajectory than what we’re seeing above with the stocks.

Point #3: How Much will the G Man Take?

There’s little denying it, real estate investments get some pretty special tax advantages vs. most other asset classes. The US is a country based on private land ownership and I believe the government believes that citizens who invest in the land and buildings they own will lead to a strong, stable country. So they change the rules for us. Making the most of these rules takes some careful planning, but if you were to plan it right under today’s tax laws there are ways where you could harness both 1031 exchanges and depreciation to defer paying any taxes on quarterly distributions or capital gains until much later in your ownership of the real estate asset, if at all. With a stock dividend however, your brokerage will be sure to let you know how much earned taxable income you’ve received on a form 1099-DIV. Both to you… and the IRS. The takeaway is, if you invest in real estate and you plan intelligently, you’re going to be keeping a lot more of your returns in your bank account.

As we continued discussing these points in more detail and found some solid data points, he eventually came around and conceded on the points above. While it’s sometimes difficult and/or laborious to compare various investments across different industries and asset classes, we hope this illustrates a few key points to collect accurate data for and compare. What are other factors you consider before you put your money to work? I’d love to discuss, feel free to connect!

Andrew Campbell is a native Austinite and Managing Partner at Wildhorn. He is a real estate entrepreneur who first broke into the business in 2008 as a passive investor. In 2010 he transitioned into active investing and management of a personal portfolio that grew to 76 units across Austin and San Antonio. He earned his stripes building and managing his personal portfolio before founding Wildhorn Capital and focusing on larger multifamily buildings. At Wildhorn, he is focused on Acquisitions and maintaining Investor Relations, utilizing his marketing and communications background to build long-term relationships.