Market Reflections and Forecasts from the 2024 CBRE Multifamily Conference

Andrew Campbell

June 28, 2024

Amidst spring thunderstorms, Wildhorn had the privilege of attending CBRE’s Annual Spring Multifamily Conference in Austin, TX. The conference was well attended by professionals from across the real estate industry. The first half of the day was spent on reflection, and the second half was optimistic about what lies ahead. Heading into the conference, we expected to hear a lot about underlying economic conditions, investor sentiment, and emerging trends. (Please see below for more detailed notes and figures from the conference and some additional thoughts.)

CBRE forecasted modest GDP growth with no anticipated recession, easing inflation, and potential interest rate cuts in 2024. We largely align with CBRE’s in-house view, but we feel that the economy, in general, is in a less robust condition than it appears today. Frankly, there are significant paper losses in the current market that have not yet been realized. We have not seen these significant losses because lenders, sponsors, and equity groups have thus far worked well together to solve any issues and extend project hold periods.

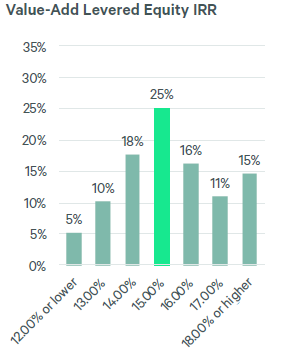

The investor sentiment survey revealed several notable items. First, the survey indicated a drop in stabilized cap rate expectations from a survey conducted at the beginning of the year. Second, there was also a noticeable shift towards offensive market participation. This offensive shift focuses on newer properties in less supply-exposed submarkets. Third, value-add equity IRR expectations increased to 15.30%. This is not surprising given the current cost of preferred equity, and we don’t expect it to drop any time soon. Investors typically achieve these IRRs through 5-year fixed agency financing where the investor is buying down the term of the loan and/or the rate, and cap rate compression. Finally, respondents expect the recovery to peak pricing to occur in 46.45 months. This recovery period fits perfectly with why investors are seeking 5-year financing with the option to exit early versus longer-term options. Investors participating in the survey appear to be practicing what they preach because we have seen several deals that fit the mold of a desired asset trade (Park on Brodie, Vineyard Hills). These assets were both built after 1990 and are in supply-constrained areas within the Austin MSA. Both deals were awarded at very competitive prices to national players.

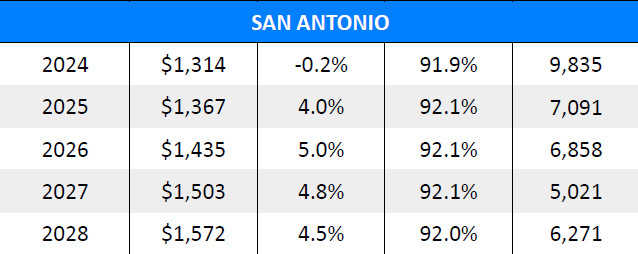

The conference concluded with a discussion on emerging trends and market projections based on data from CBRE, Yardi, and John Burns Research. The first notable item was a discussion on the recovery in occupancy and rent growth in Austin and San Antonio. The data from the conference suggests that both occupancy and rent growth are anticipated to improve in 2025. Second, there is a significant affordability gap between the cost of home ownership and renting. Tying into the discussion of home ownership, the topic quickly shifted to the rise of Build-to-Rent (BTR) properties. This emerging asset class is driven by trends such as work-from-home, declining homeownership affordability, household formation growth, and demographic shifts. BTR is a unique segment within residential real estate investment, offering a single-family home lifestyle at a cost slightly above apartments but below homeownership. Wildhorn believes the cost disparity between ownership and renting will decrease through a combination of rising rents, falling interest rates, or declining home prices. In our opinion, there is support for housing prices to remain relatively high, interest rates to decline, and rents to increase because current interest rates are restrictive, the housing market remains under-supplied, and the future delivery schedule for apartments is a short-term issue and has fallen significantly from the recent peak. These conditions, along with increased institutional ownership focused on the BTR segment, will create excellent opportunities for those who can create desirable BTR communities.

The CBRE Multifamily Conference Key Points:

Preconference Multifamily Client Survey:

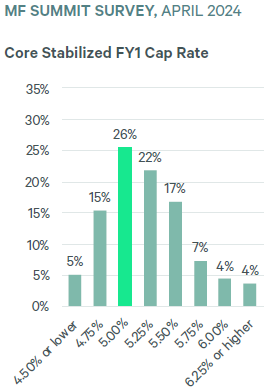

The Multifamily Client Survey conducted at the Multifamily Summit in April 2024 garnered 154 unique client responses, offering valuable insights into industry sentiment and expectations. Key findings include:

- Core stabilized FY1 Cap Rate expectations dropped 16 basis points from January to 5.22% in April.

- ~80% of respondents centered around 4.75% to 5.5%.

- Market participants feel more active with 79% percent of respondents indicating they are on the offensive. From a central Texas perspective market most institutional participants are focused on specific products that are typically 2000’s or newer in submarkets with less exposure to future supply.

- Value-Add equity IRR expectations rose to 15.30%. This is up from ~12% in January of this year.

- This does not surprise us as equity investors should expect returns that are higher than what the preferred equity market is projecting today.

- But how are they arriving at these returns? Most respondents are focused on 5-year fixed agency financing and some are showing a willingness to underwrite cap rate compression over the life of their hold.

- Expectations for recovery of peak pricing averaged 46.45 months which is in line with an expected 5-year hold period.

CBRE Economic Projections:

CBRE provided optimistic economic projections, highlighting:

- They are not projecting a recession anymore and are now projecting positive, but modest GDP growth in the near term.

- Anticipated easing of inflation in 2024, with potential for two 25 basis point cuts in interest rates.

- CBRE economists expect the easing of 10-year treasury yields to ~3% over the next. The current projection would mean that 10-year treasury yields are expected to be about 100 basis points higher than the long-term average between 2009 to 2019.

- Wildhorn does not have a projection on where the 10-year treasury will average over the long term, but we generally agree that they will be higher than the 2009 – 2019 average.

- Cap rates are projected to peak at 6% this year before stabilizing above 5% long term.

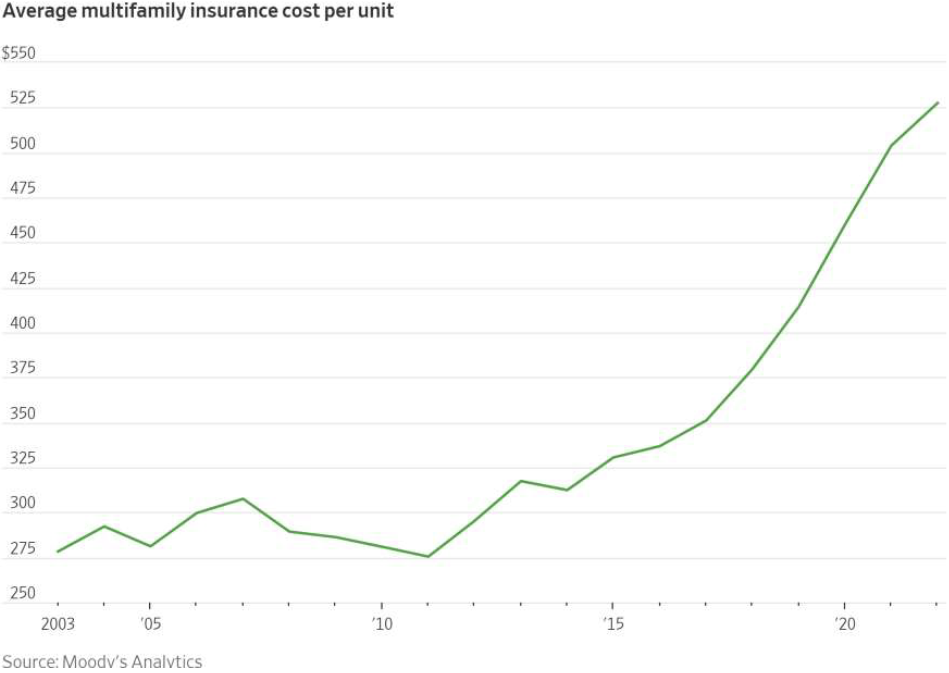

- Recognition of dramatic rise in operating expense burdens (especially insurance and personnel costs) on multifamily operations and minimal impact of geopolitics on the cycle.

Yardi / John Burns Data:

Insights from Yardi and John Burns data included:

- Projected recovery of occupancy and rent growth in Austin and San Antonio starting in 2025.

- Analysis of the affordability gap between mortgage payments and rent, with implications for single-family rentals (SFR).

- The average monthly mortgage payment in Austin is $3,002 while the average monthly rent payment is $1,755. A difference of almost $1,250 per month!

- We expect that the gap between the average monthly mortgage payment to shrink through a combination of lower mortgage costs and higher rent.

- In our opinion, there is support for housing prices to remain relatively higher, interest rates to decline, and rents to increase because the housing market remains undersupplied, current apartment supply is a short-term issue, and the future delivery schedule for apartments has fallen significantly from the recent peak.

- We expect that the gap between the average monthly mortgage payment to shrink through a combination of lower mortgage costs and higher rent.

- Economists at CBRE are generally excited about the future of Build-to-Rent (BTR) properties, noting institutional ownership benefits because of their access to greater resources, maintenance, and amenities.

- The average monthly mortgage payment in Austin is $3,002 while the average monthly rent payment is $1,755. A difference of almost $1,250 per month!

- Identification of demand drivers for SFR include work-from-home trends, declining home ownership affordability, household formation growth, and demographic shifts.

- Qualities of future BTR developments should include amenities (on-site maintenance, community, parking, storage, privacy, yard, pool, clubhouse), smart tech integration, and design considerations for accommodating frequent moving.

Andrew Campbell is a native Austinite and Managing Partner at Wildhorn. He is a real estate entrepreneur who first broke into the business in 2008 as a passive investor. In 2010 he transitioned into active investing and management of a personal portfolio that grew to 76 units across Austin and San Antonio. He earned his stripes building and managing his personal portfolio before founding Wildhorn Capital and focusing on larger multifamily buildings. At Wildhorn, he is focused on Acquisitions and maintaining Investor Relations, utilizing his marketing and communications background to build long-term relationships.